In federal court on Monday, a former employee of Stericycle Inc., which is based in Lake Forest, entered a plea of not guilty to accusations that he and his mother illegally gained over $300,000 in profits combined by trading on non-public insider information.

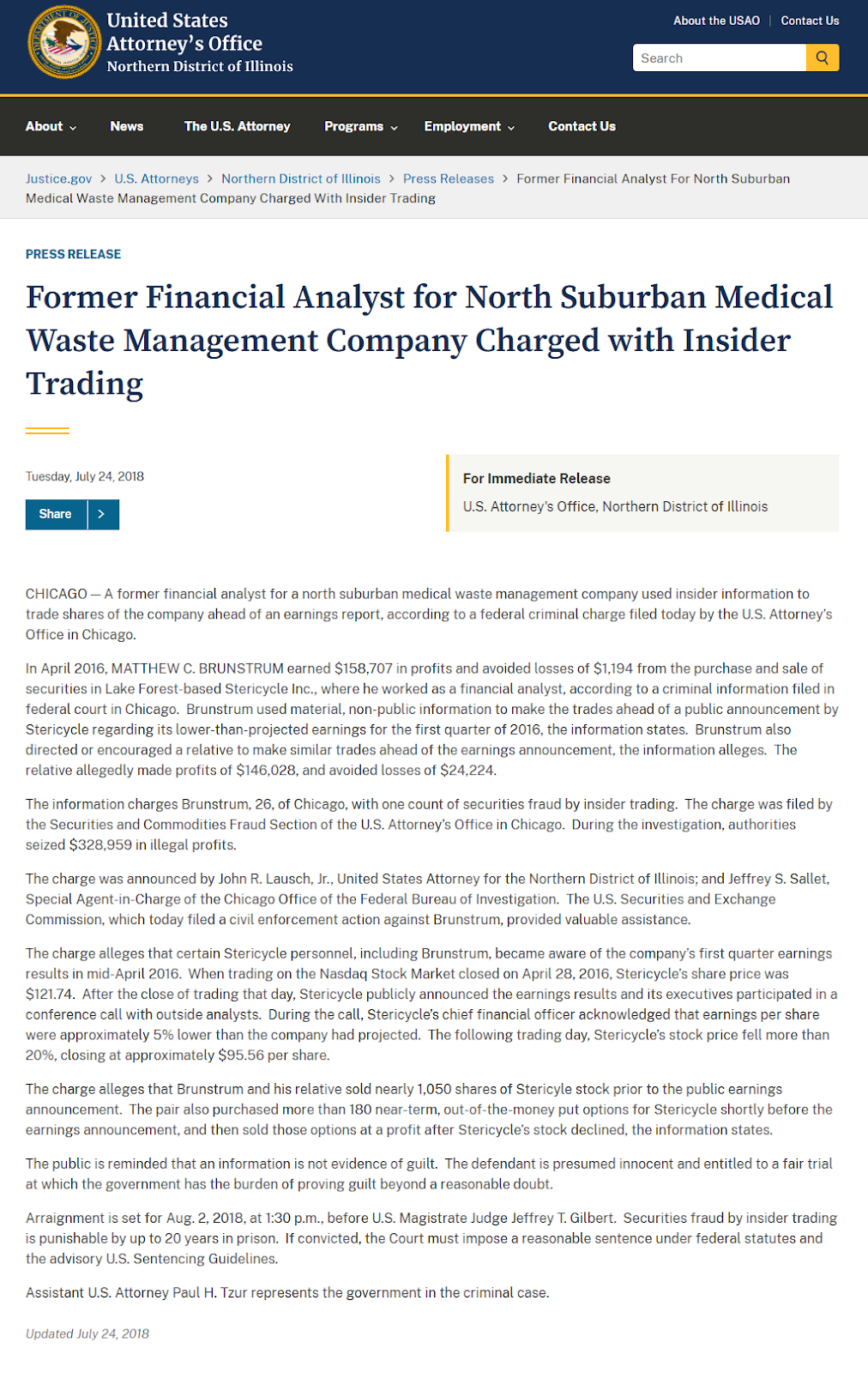

According to the records filed with the court, Matthew Brunstrum, who is 26 years old and lives in Chicago, was charged on July 24 with trading in the stock and options of the medical waste disposal company in 2016. This occurred before a public report that detailed the company’s dismal performance for the first quarter of 2016.

The charges were submitted to the United States District Court for the Northern District of Illinois Eastern Division by the securities fraud unit found inside the United States Attorney’s Office.

“As an employee of Stericycle, Brunstrum owed a fiduciary duty and other duties of trust and confidence to Stericycle to maintain the confidentiality of any material, non-public information he learned and obtained during his employment,” the federal government’s criminal complaint states. Brunstrum was obligated to keep the information confidential.

Brunstum, on the other hand, is accused of using the advance knowledge of the first quarter profits to begin selling business stocks and “directing or encouraging” his mother, Susan, to do the same. This is according to the complaint.

According to the criminal complaint, “[Matthew] Brunstrum made illegal profits of approximately $158,707 and also avoided losses of approximately $1,194 as a result of these transactions.” Brunstrum also avoided losses of roughly $1,194 overall.

In the criminal complaint, Susan Brunstrum, who is 56 years old, is only referred to as “Individual A.” The complaint states that she “made profits of approximately $146,028 and also avoided losses of approximately $24,224.”

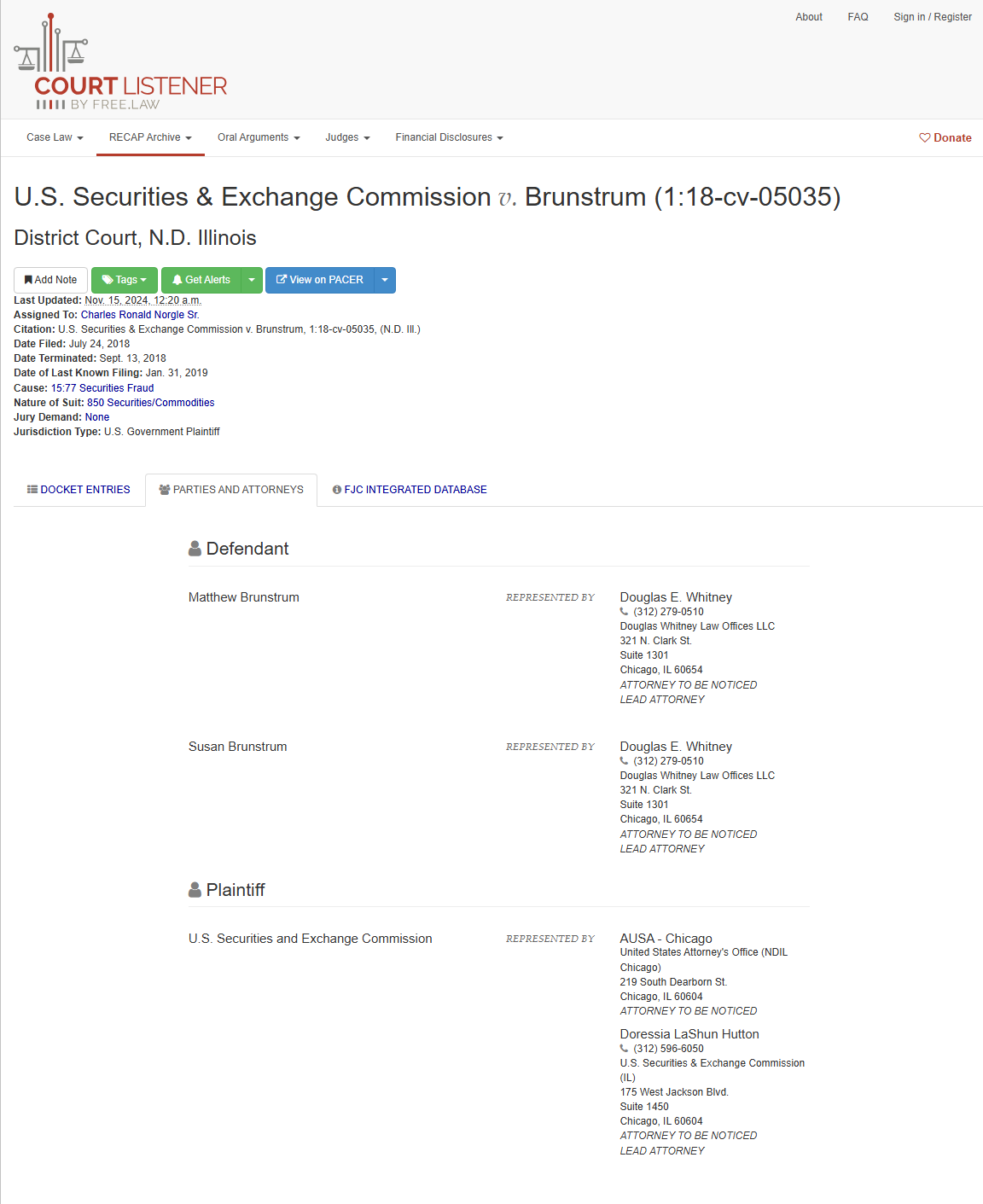

In addition to the criminal accusations that were brought against Brunstrum, the United States Securities and Exchange Commission also brought a civil case against him and his mother in federal court on the same day that the criminal charges were brought.

A complaint filed with the Securities and Exchange Commission states that Matthew Brunstrum was employed by Stericycle as a financial analyst beginning in November 2014 and continuing until April 2017, when he was terminated due to his refusal to take part in an internal enquiry of insider trading.

According to the complaint filed with the SEC, Matthew Brunstrum’s father, who was married to Susan Brunstrum, worked as an executive at Stericycle until his death in the year 2000.

The allegations against Matthew Brunstrum include the use of information that is not available to the public prior to the announcement made on April 28, 2016, that Stericycle will fall short of the profit forecasts of analysts by four cents per share. Following that, he informed his mother, who proceeded to sell her stock.

According to facts contained in both the criminal and civil accusations, the stock market ended the following day at $95.56 per share on the NASDAQ stock exchange. This represents a decrease of 22 percent from its previous closing price of $121.74 per share.

Brunstrum and his mother are being asked by the Securities and Exchange Commission to “disgorge all of their ill-gotten” profits.

If Matthew Brunstrum is found guilty of the criminal accusations, he could be sentenced to a maximum of twenty years in jail.

He suggested that calls be directed to attorney Doug Whitney, who stated that he is representing both Brunstrums currently.

SEC Charges Funeral Financing Company in $55 Million Ponzi Scheme

At least 150 investors were reportedly taken advantage of by a Ponzi scheme that was worth $55 million, and the Securities and Exchange Commission has filed charges against a collection of firms and their principals.

According to the complaint filed by the Securities and Exchange Commission (SEC), Daniel Rudden and a group of companies operating under the name Financial Visions defrauded investors by promising them annual returns of 12% or more. These companies issued promissory notes to fund their operations in short-term financing for funeral services and related expenses to fund their operations.

In or around the year 2001, Financial Visions was established with the purpose of providing life insurance assignments to family members of deceased individuals. These assignments are intended to cover funeral expenditures before the payout of the decedent’s life insurance policy.

According to the Securities and Exchange Commission (SEC), the businesses’ stated business of “life insurance assignments” consisted of funding funeral and related expenses in exchange for reimbursement of those expenses, in addition to a five percent compensation fee that was secured by a deceased person’s life insurance policy.

A complaint has been filed alleging that Rudden has been using funds from new investors to pay interest and redemptions to current investors since 2010 or 2011. Additionally, the complaint claims that Rudden has disguised the true financial performance and condition of the Financial Visions companies.

In addition, the complaint asserts that Rudden continued to portray the company as profitable to both current and potential investors, despite the fact that he was aware that he was operating a Ponzi scheme.

As an illustration, when the Financial Visions Companies stopped providing interest payments to investors, Rudden issued an email to investors explaining that this was due to a huge capital call because of a “inordinate number of deaths of our investor group (12 people with over $2,000,000 invested).” His email was sent to investors.

Rudden confessed in an email that the Financial Visions Companies had been operating as a Ponzi scheme from 2010 or 2011, and this admission was made around the month of July 2018.

“I come up with no defence. Throughout the process, I made a deliberate decision to continue receiving money in order to maintain the interest rate. It was at that point that it turned into a Ponzi scheme,” he stated in the email.

Having achieved an immediate asset freeze and other forms of relief, the Securities and Exchange Commission (SEC) is now requesting permanent injunctions, disgorgement along with prejudgement interest, and penalties.

Moreover, the Securities and Exchange Commission (SEC) has listed three entities as relief defendants. The SEC asserts that these entities were controlled by Rudden and that they received investor monies from the alleged Ponzi scheme.

A charge of misrepresenting his disciplinary history to customers has been brought against the advisor by Galvin.

A registered broker-dealer and investment adviser representative was charged with spreading misleading information to clients and prospective clients on his website, according to Secretary of State William Galvin, who is the most senior securities regulator in the state of Massachusetts.

A number of assertions that Alan Siegel made on his website about his disciplinary record in the securities sector were obviously untrue. The majority of his clients are retirees or those who are getting close to retirement.

According to the administrative complaint that was submitted by Galvin’s Securities Division, Siegel had consistently issued a statement on his website under the headline “Reliability Report” for a number of years. In this statement, he asserted that he had never been the subject of a complaint lodged against him by any firm, organisation, or regulatory agency. Siegel went to the extent of highlighting the word “never” by writing it in all capital letters and underlining it. This was done in order to attract the attention of the reader.

In point of fact, according to his BrokerCheck record, Siegel has been accused of shoplifting a pair of sneakers in 1970, when he was just 17 years old. These clients have filed three complaints against him, alleging that they have suffered damages amounting to hundreds of thousands of dollars. In answer, he stated that he had a limited recollection of the incident and that he did not remember being charged with anything.

G.A. Repple & Co., Siegel’s employer, was also accused of failing to oversee its agent in the lawsuit that was filed against them.

In the complaint, it is stated that G.A. Repple & Co. did not provide Siegel and his website with significant review and oversight, but rather just rubber-stamped the information. The fact that G.A. Repple had paid for settlements with customers who had accused Siegel of breaching his fiduciary duties, offering assets that were not suitable for them, and failing to disclose crucial facts meant that he was well aware of the complaints that had been lodged against Siegel.

Specifically, the office of Galvin is requesting that Siegel and G.A. Repple be subject to a cease and desist order, as well as a censure, sanctions, and an administrative fee.

A former trader has reached a settlement with the Securities and Exchange Commission (SEC) regarding an insider trading scheme that was worth $1.1 million.

A former professional trader has been accused by the Securities and Exchange Commission (SEC) with allegedly taking part in a conspiracy of insider trading that involved an investment banker, his father, and a serial insider trading scam that resulted in illegal profits of $1.1 million.

According to the complaint filed by the Securities and Exchange Commission (SEC), Robert Stewart enlisted the assistance of his buddy Richard Cunniffe, who is a professional trader, in order to execute trades based on confidential information that Stewart obtained from his son Sean Stewart, who is an investment banker.

According to the Securities and Exchange Commission (SEC), Cunniffe utilised the information to execute trades in his personal accounts, resulting in about $1.1 million in illegal proceeds that he then distributed to Robert Stewart.

A complaint filed by the Securities and Exchange Commission (SEC) accuses Cunniffe of violating antifraud provisions of federal securities laws.

In addition to cooperating with the investigation and having previously entered a guilty plea to criminal charges, Cunniffe has agreed to resolve the civil accusations that have been brought against him by the SEC. Injunctive relief, disgorgement, and interest are all ordered as part of the settlement, which is contingent to the approval of the court. However, there is no punishment.

As a result of Cunniffe’s guilty plea, the Securities and Exchange Commission (SEC) prohibited him from working in the securities sector.

An Insider Trading Charge Has Been Filed Against a Financial Analyst and His Mother by the SEC

Matthew Brunstrum, who had previously worked as a financial analyst at Stericycle Inc., was charged with insider trading by the Securities and Exchange Commission. Additionally, he was accused of providing information to his mother, who was themselves charged with insider trading.

In the complaint filed by the Securities and Exchange Commission (SEC), it is alleged that Matthew Brunstrum obtained knowledge from his job in April 2016 that Stericycle’s first-quarter 2016 financial results would be significantly worse than had been anticipated. Brunstrum then utilised this material nonpublic information to engage in trading in Stericycle securities prior to the company’s earnings announcement on April 28, 2016.

Additionally, the complaint asserts that Matthew Brunstrum divulged information on Stericycle’s earnings to his mother, who then proceeded to trade based on that revealed information.

The shares of Stericycle had a decline of $26.18 the day after the company released its financial results for the first quarter, resulting in a loss of over 22% of its value. Matthew Brunstrum and Susan Brunstrum are accused of avoiding losses and earning profits in the sum of $159,904 and $170,252 respectively as a result of their illicit trading, according to the complaint filed by the Securities and Exchange Commission (SEC).

Matthew Brunstrum and Susan Brunstrum both agreed to be permanently enjoined from future violations of antifraud provisions of the securities laws. Additionally, they agreed to pay disgorgement equal to each of their ill-gotten earnings in addition to prejudgement interest.

This agreement was made without either of them admitting or disputing the claims. The amounts of the civil penalties shall be decided only by the court. The settlements are contingent upon the approval of the court.

The former spouse and friend of the “Frack Master” has been ordered by the court to return $1.12 million

According to separate orders issued by a federal district court in Texas, the ex-wife of Chris Faulkner, who self-proclaimed himself to be the “Frack Master,” and one of his pals were required to hand over a sum of money that exceeded $1.12 million.

The court issued a final judgement against Tamra Freedman, who was Faulkner’s ex-spouse, ordering her to return $900,000. Additionally, the court issued a final judgement against Jetmir Ahmedi, ordering Ahmedi to return $222,000 in his possession.

In order to recover ill-gotten earnings that they received from Faulkner, the Securities and Exchange Commission (SEC) identified Freedman and Ahmedi as relief defendants. Faulkner was one of the defendants that the SEC sued together with 11 other defendants for their roles in an alleged oil-and-gas securities fraud scheme that was worth $80 million.

By reaching a settlement with the Securities and Exchange Commission, Freedman and Ahmedi did not accept or deny the claims.

A charge of failure to protect customer information has been brought against Mizuho Securities by the SEC

A charge was brought against Mizuho Securities USA LLC by the Securities and Exchange Commission (SEC) for failing to protect information regarding stock buybacks by its issuer clients.

According to the Securities and Exchange Commission (SEC), Mizuho failed to maintain and implement rules and procedures that were intended to prevent the misuse of material nonpublic information. These policies and procedures included the requirement that workers are required to keep client information confidential and the maintenance of effective information barriers between different trading desks.

Mizuho has reached an agreement to settle the allegations and will then pay a penalty of $1.25 million. According to the order issued by the SEC, throughout a period of two years, Mizuho traders routinely provided material nonpublic customer buyback information to other traders as well as to clients of Mizuho’s hedge fund. The identity of the party that placed the order, the size of the transaction, the limit price, and indicators that the orders were repurchase orders were all included in this information.

This kind of information was frequently exchanged between trading desks, despite the fact that throughout the relevant time period, Mizuho completed over 99.8 percent of all repurchase orders by utilising algorithms, rather than through trader-negotiated open market trades.

Mizuho gave its assent to the order that imposed a 1 million dollar penalty, a censure, and an order to cease and desist from committing or causing any future violations. This was done without admitting or contesting the findings of the Securities and Exchange Commission (SEC).

A Silicon Valley executive’s insider trading has been discovered by the SEC

To settle charges that he generated over $200,000 in illegal profits by trading on inside knowledge in advance of three dismal earnings reports by the company, a senior executive at a Silicon Valley fibre optics company agreed to settle, according to a statement issued by the Securities and Exchange Commission (SEC).

This case originates from the Analysis and Detection Centre of the Securities and Exchange Commission’s Market Abuse Unit. This centre employs data analysis methods to identify potentially suspicious trends, such as trading that is improbably successful in advance of earnings announcements, throughout the course of time.

Yao Li, in his capacity as vice president of Technology at Alliance Fibre Optic Products, Inc. (AFOP), was informed, over the course of regular meetings with AFOP’s senior executives, that the firm was likely going to miss its sales guidance in three distinct quarters between the years 2014 and 2015. This information was disclosed in compliance with the order issued by the SEC.

Li traded on this inside information by short selling AFOP shares for gains and selling AFOP shares he already owned in order to minimise losses prior to these disclosures, as stated in the order issued by the New York Securities and Exchange Commission (SEC). Short selling was expressly prohibited for workers of AFOP, according to the Securities and Exchange Commission (SEC).

A disgorgement of $196,200, prejudgment interest of $23,100, and a penalty of $196,200 are all had to be paid by Li, bringing the total amount to $415,500. In addition, Li consented to a five-year period during which he would be barred from serving in any capacity as an officer or director of a publicly traded business.

The Shocking Reality Behind the Ponzi Scheme

National Trends & Enforcement

- In 2023, authorities uncovered 66 Ponzi schemes nationwide, causing nearly $2 billion in potential investor losses.

- This follows 57 schemes in 2022 (≈ $5.3 billion in losses) and 60 schemes in 2020 (≈ $3.25 billion lost) .

- The decline in the number of schemes from 60 in 2019 to 34 in 2023 marks the lowest since 2008 ponzitracker.com, though losses remain high.

Enforcement Activity

- NASAA reports that state and territorial regulators handled 8,768 investigations in 2023, leading to 1,186 enforcement actions—including 121 criminal and 102 civil actions.

- The SEC continues tackling high-profile cases—its FY 2024 enforcement report highlights significant activity against billion-dollar Ponzi schemes.

Prominent Case Examples

- Francius Marganda (Apr 2025): U.S. citizen convicted in NY for a $24.5 million scheme targeting the Indonesian‑American community; received 18 years in prison.

- Russell Todd Burkhalter (Aug 2024): SEC charged him with running a $300 million real estate Ponzi scheme affecting 2,000+ investors; assets frozen.

- Tom Girardi (Aug 2024): Disbarred lawyer found guilty of a $15 million Ponzi scheme through embezzlement from clients, faces up to 20 years.

- Ruja Ignatova (“Cryptoqueen”) is still at large for the infamous $4 billion OneCoin crypto Ponzi; a co-conspirator received a 20-year sentence.

Crypto-Related Ponzi Schemes

- Reports indicate a surge in crypto investment fraud; IC3 logged more than 69,000 cryptocurrency fraud complaints in 2023.

- High-profile crypto scams like OneCoin, HyperVerse (alleged $1.7–1.9 billion), and Celsius emphasize the proliferation of cryptocurrency Ponzi and pyramid schemes.

Whistleblowers & Investor Warnings

- SEC whistleblower tips related to offering fraud rose steadily: from 16% in FY 2021 to 21% in FY 2024.

- The FTC reported that consumers lost $5.7 billion to investment scams in 2024—more than any other category.

Takeaways

- Ponzi activity remains common, with ~60 schemes uncovered annually and billions in losses.

- Enforcement is robust, involving federal and state agencies, leading to high-profile arrests and convictions.

- Crypto is a growth area—both in scheme volume and total dollar value lost.

- Whistleblower channels and consumer reporting are on the rise, essential for detecting fraud.